SECTOR REPORT SYNTHESIS

Argentine-German bilateral trade: horizon of the commercial relationship

This paper analyses the evolution of bilateral trade between Argentina and Germany during the period 2003-2023 in order to characterize and identify the main specialization patterns consolidated over the last two decades. The study focuses particularly on the sectoral and technological composition of the exchange, assessing the place Germany occupies within Argentina's import structure and the implications this relationship has in terms of industrial and technological dependency.

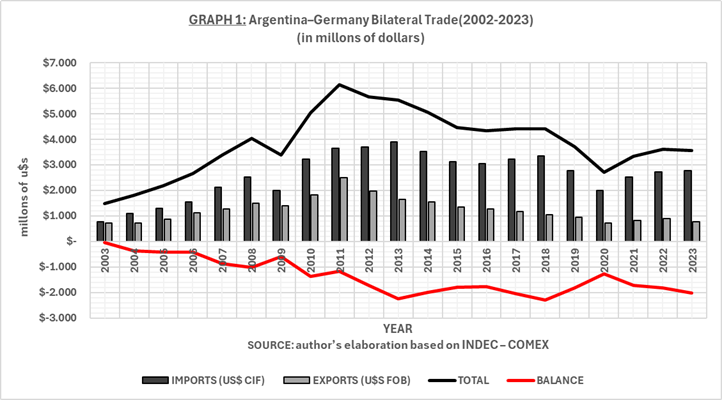

Between 2003 and 2023, Argentine-German bilateral trade grew by approximately 139% in nominal terms, rising from USD 1.487 billion to USD 3.551 billion annually. During the period, trade reached peaks above USD 6.1 billion and accumulated more than USD 95 billion in commercial operations. However, the absolute growth of trade was not accompanied by a significant modification of the bilateral structure. Throughout practically the entire period analysed, Argentina maintained persistent trade deficits with Germany, accumulating a negative balance of more than USD 28 billion.

The study identifies a structural continuity that cuts across different macroeconomic cycles and political orientations. Both during the economic expansion of the post-convertibility period and during later stages of external restriction, trade opening or exchange-rate administration, the general composition of bilateral exchange remained relatively stable. Argentina exported mainly primary goods and low-technology manufactures, while Germany consolidated its position as a supplier of complex industrial goods, specialized machinery and embedded technology.

The research shows that Argentina's export structure to Germany presents high sectoral concentration. During much of the period, the ten main chapters accounted for between 85% and 90% of total exports. The main items correspond to meat and edible offal (HS02), metalliferous ores (HS26), food-industry residues (HS23), organic chemicals (HS29), wool (HS51), dairy products (HS04) and certain segments linked to the agro-industrial complex.

Chapter HS02 - meat and edible offal - represented approximately 24% on average of Argentine exports to Germany during the period. In certain years, the meat complex exceeded 30% of total exports. The second major export block corresponded to metalliferous ores and concentrates, particularly copper, lithium and other resources linked to extractive chains.

Industrial exports of greater relative complexity had a much more limited presence. Mechanical machinery and capital goods (HS84) represented only 2.6% on average of Argentine exports to Germany. Precision instruments and medical technology (HS90) hovered around 1.5%, while electrical machinery (HS85) and pharmaceutical products maintained marginal shares.

Argentina's import structure from Germany presents a radically different configuration. Imports are concentrated mainly in mechanical machinery and industrial engineering (HS84), vehicles and auto parts (HS87), pharmaceutical products (HS30), electrical machinery (HS85), high-complexity chemical products and precision instruments (HS90). In general terms, these are medium-high and high-technology industrial goods.

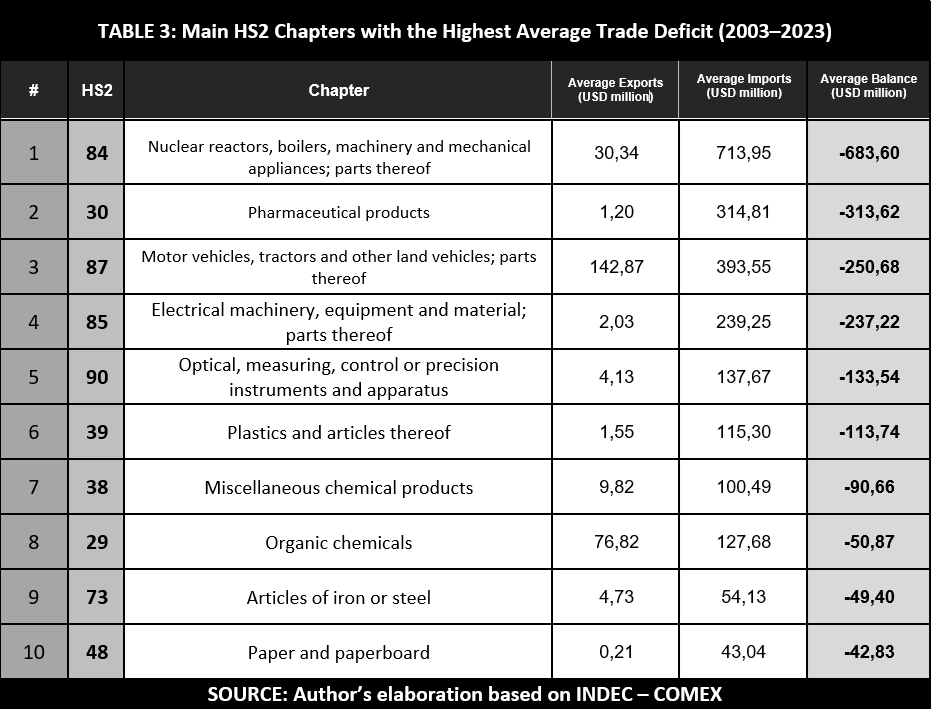

Chapter HS84 constitutes the structural core of the bilateral industrial relationship. Between 2003 and 2023, Argentina imported from Germany more than USD 15 billion accumulated in machinery and mechanical equipment, with annual averages above USD 700 million. During some years of the 2010-2017 period, imports within HS84 even exceeded USD 1 billion annually.

Argentine exports to Germany within that same chapter were comparatively insignificant, with averages below USD 30 million annually. The structural deficit associated only with mechanical machinery and industrial engineering thus exceeded USD 680 million on average per year during the period analysed.

The study also identifies a particularly high concentration of German imports in industrial segments linked to process machinery, automation, specialized industrial equipment, complex chemicals and control and precision instruments. Germany maintains relative density in positions associated with high technical specificity, long industrial life cycles and strong integration between engineering, maintenance and technical support.

Within Chapter HS90 - precision instruments and medical technology - Germany also occupies a stable position as a supplier of analytical equipment, medical instruments, diagnostic devices and hospital technology. In certain specific segments, such as chromatography, spectrometry, analytical instruments and specialized medical equipment, the German presence remained practically constant throughout the period analysed.

The analysis shows that the bilateral imbalance does not simply respond to differences in trade volume, but to a structural gap in productive and technological capabilities. Argentina's main surpluses are generated in goods associated with natural resources and agro-industrial chains, while deficits are concentrated precisely in those sectors that require greater accumulation of knowledge, R&D investment and complex industrial integration.

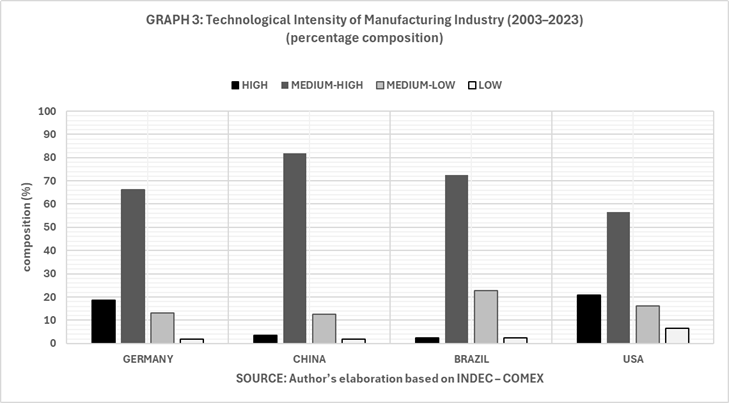

The research also incorporates a classification by technological intensity that makes it possible to specify the nature of the bilateral asymmetry. More than 70% of Argentine exports to Germany correspond to low-technology goods or natural-resource-based manufactures. By contrast, imports from Germany are concentrated predominantly in medium-high and high-complexity industrial manufactures.

In relative terms, Germany occupies a singular position within Argentina's import structure: it explains more than 12% of the aggregate trade deficit Argentina maintains with its four main industrial partners (China, Brazil and the United States), although it represents approximately 4.8% of total imports from this group.

The paper argues that Germany's singularity does not lie only in the absolute volume of trade, but in the specific technological function it performs within Argentina's productive apparatus. Germany maintains an insertion particularly associated with specialized machinery, automation, complex industrial chemistry, precision engineering and productive equipment of high technological density.

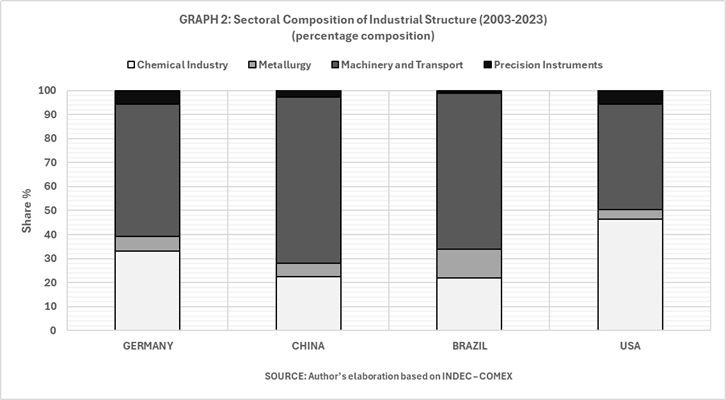

The comparison with other industrial partners reveals important differences in insertion profiles. China is increasingly consolidating itself as the dominant supplier by volume, particularly in standardized machinery, industrial electronics and scale manufactures. Brazil maintains a structure more associated with industrial manufactures of intermediate technological density, especially within automotive chains and regional industrial goods. The United States retains relevant positions in pharmaceuticals, specialized chemistry and certain high-technology segments. Germany, by contrast, transversally combines industrial machinery, complex chemistry and precision instruments within a relatively diversified and technologically dense structure.

The temporal persistence of this bilateral structure spans periods of foreign-trade administration, stages of import liberalization and different macroeconomic crises without substantially modifying the observed specialization pattern. The relative stability of the relationship suggests the existence of a deeply consolidated industrial structure, where certain segments of Argentina's productive apparatus continue to depend on equipment, technology and industrial inputs from economies of greater relative complexity.

The study also identifies that German exports to Argentina do not consist only of isolated physical goods. In multiple industrial segments, particularly machinery and industrial engineering, imported goods simultaneously incorporate technical support, maintenance, spare-parts provision, operational updating and technological assistance. Dependency is therefore not limited to the initial acquisition of equipment, but extends through much of the operational cycle of the imported good.

In structural terms, the paper concludes that the Argentine-German bilateral relationship reproduces a relatively stable configuration in which technological capabilities, industrial value added and the production of complex goods remain mainly concentrated on the German side, while Argentina maintains an export profile associated predominantly with natural resources and manufactures of lower technological density.

However, the research argues that precisely this density of exchange in certain industrial sectors makes it relevant to analyse possible margins for productive articulation or selective technological cooperation. The existence of relatively stable commercial relationships in industrial machinery, medical technology, specialized chemistry and precision instruments raises the possibility of exploring limited mechanisms of technology transfer, local supplier development or institutional cooperation in specific segments of the bilateral relationship.

Any strategy aimed at partially modifying the structure of the relationship requires abandoning exclusively commercial interpretations of bilateral exchange. The central problem does not lie only in the negative trade balance, but in the persistence of a structural gap in technological, productive and industrial capabilities between the two economies. In this sense, future stages of research will move toward higher levels of sectoral disaggregation (HS4 and HS6) in order to identify specific productive chains, relative specialization patterns and possible niches of industrial cooperation within a relationship recognized as asymmetric.

This synthesis was prepared for CEIBO. The full article is available in Spanish upon request: contact@ceibo-berlin.de